Payroll Integration

Payroll Integration

Different ways payroll integration can be achieved

In today’s fast-paced business environment, efficiency is paramount. For companies to stay competitive, integrating various systems into their payroll software can streamline operations, reduce errors, and save valuable time and resources.

Here’s a closer look at the different ways and systems that can seamlessly integrate with payroll software to create a more efficient, effective, and user-friendly experience.

1. Human Resource Management Systems (HRMS)

Why Integrate?

HRMS integration with payroll software automates the flow of employee data, reducing redundancy and errors. This integration ensures that any changes in employee status, benefits, remuneration awards, workforce planning, or recruitment are instantly reflected in payroll processing.

Key Benefits:

- Real-time Data Synchronization: Automatically updates payroll with new hires, terminations, and changes in employee information.

- Enhanced Accuracy: Minimizes manual data entry which reduce the risk of errors.

- Streamlined Onboarding: Simplifies the onboarding process by automatically enrolling new employees in payroll.

2. Time and Attendance Systems

Why Integrate?

Integrating time and attendance systems with payroll software ensures that employee hours are accurately tracked and paid, avoiding discrepancies, and ensuring compliance with labour laws.

Key Benefits:

- Automated Time Tracking: Automatically transfers clock-in and clock-out data to payroll.

- Compliance Assurance: Helps maintain accurate records for labour law compliance.

- Improved Productivity: Reduces administrative burden by allowing HR and payroll staff to focus on more strategic tasks.

3. Accounting Software

Why Integrate?

Linking payroll software with accounting systems ensures that payroll expenses are accurately recorded, and financial statements are up-to-date ad accurate facilitating a comprehensive view of the company’s financial health.

Key Benefits:

- Seamless Financial Reporting: Automatically updates accounting records with payroll data.

- Improved Financial Accuracy: Reduces the risk of errors in financial statements.

- Simplified Reconciliation: Streamlines the process of reconciling payroll expenses with bank statements.

4. Employee Benefits Management Systems

Why Integrate?

Integration with benefits management systems ensures that payroll deductions for benefits are accurate and up to date, facilitating smoother administration of employee benefits.

Key Benefits:

- Accurate Deductions: Ensures correct deductions for health insurance, retirement plans, and other benefits and that the correct monthly payments are made to the administrator.

- Enhanced Employee Satisfaction: Provides employees with clear, accurate information about their benefits.

- Streamlined Administration: Simplifies the process of managing employee benefits.

5. Customer Relationship Management (CRM) Systems

Why Integrate?

For companies where payroll impacts customer billing, integrating CRM systems with payroll software can ensure that client billing is accurate and timely.

Key Benefits:

- Accurate Billing: Ensures client invoices reflect actual labour costs.

- Enhanced Client Trust: Builds trust with clients through accurate and transparent billing.

- Operational Efficiency: Reduces the time spent on manual data entry and reconciliation.

6. Project Management Software

Why Integrate?

Integrating project management software with payroll systems can help track labour costs by project or cost centre therefore improving project budgeting and profitability analysis.

Key Benefits:

- Precise Cost Tracking: Links labour costs directly to specific projects.

- Improved Budgeting: Enhances project cost forecasting and control.

- Profitability Analysis: Helps determine the profitability of projects by providing accurate labour cost data.

7. Statutory Filing Systems

Why Integrate?

Integrating tax filing systems with payroll software automates the preparation and submission of payroll taxes, ensuring compliance with local tax regulations. We can manage the most complex integration to the simplest communication with revenue authorities throughout the African continent.

Key Benefits:

- Automated Statutory Filing: Automatically calculates and submits payroll statutory obligations.

- Regulatory Compliance: Ensures adherence to tax laws and deadlines.

- Reduced Penalties: Minimizes the risk of fines or penalties due to errors or late filings.

8. Payroll Advance payments to employees

Why Integrate?

Integrating payroll with financial banking platforms will allow your employees to receive an advance of their net pay.

Key Benefits:

- Reducing payroll administration

- Reduced risk to lending third party.

- Eliminating funding requirements for the employer on payroll advances

- Improved Employee Value Proposition.

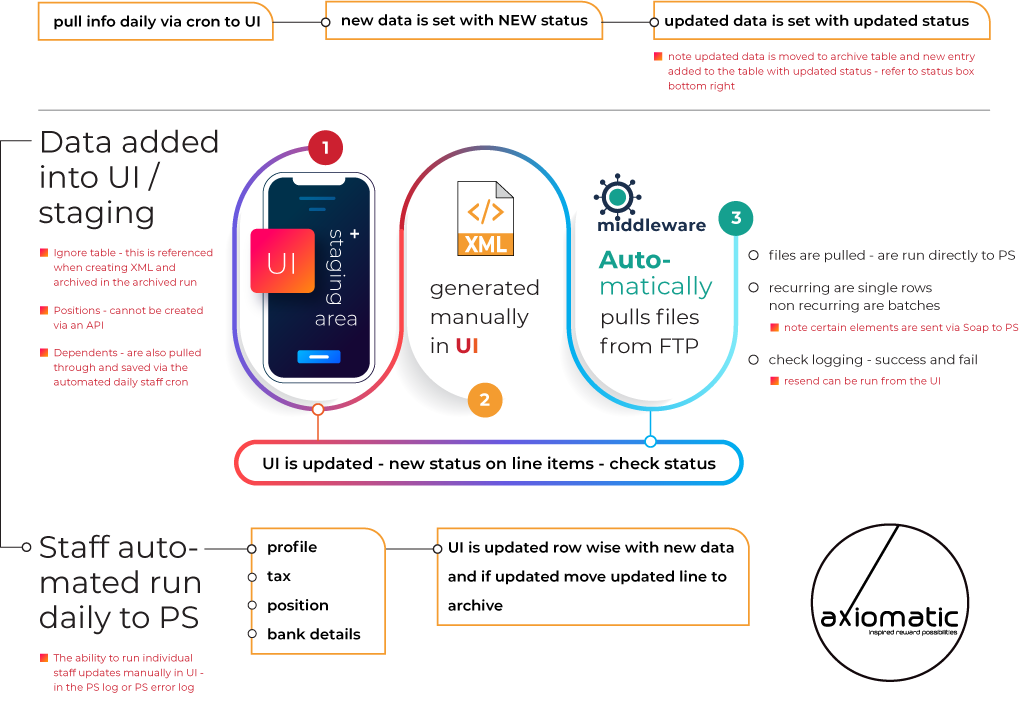

Axiomatic has significant experience integrating with other systems using API’s including the development and set-up of appropriate middleware. Previous interface projects have ranged from rather simple interfaces to custom-built solutions with a complete staging area with two bridges between various systems to ensure the data was “cleansed” and coupled with update logging, data quality validation, and consistency.

Why Integrate?

- A tailored solution is precisely aligned with the client’s specific business needs, ensuring that the solution fits perfectly into their existing workflows and processes.

- Customization allows for the optimization of the API to handle the unique demands of the client’s operations, leading to more efficient and streamlined processes. This reduces the time and effort required for integration and ongoing operations.

- Custom APIs can be designed to scale with the client’s business. As the client grows or their needs change, the API can be adjusted accordingly, ensuring that it continues to meet their requirements without requiring significant overhauls.

- Scalability can enhance performance by ensuring that the API is neither over-engineered nor underpowered, leading to faster response times and more reliable data exchange.

- By delivering precisely what the client needs without unnecessary features or complexity, customized APIs can be more cost-effective, reducing both initial implementation costs and ongoing maintenance expenses.

Conclusion

Integrating various systems with payroll software is not just a trend but a necessity for modern businesses aiming for operational efficiency and accuracy. By creating a seamless flow of information between payroll and other essential business functions, companies can reduce administrative burdens, enhance accuracy, and ultimately, improve employee and client satisfaction. Investing in these integrations can lead to significant time and cost savings, positioning your business for sustained growth and success.

With our extensive expertise in both African payrolls and powerful technology and tools, we truly believe we can deliver a single scalable solution for your integration environment in Africa.

If you would like to discuss integrations with us, please:

Payroll Integration Read More »